Last Updated: May 2026 | By Omar Al-Fayed, Senior Automotive Consultant | Category: UAE Market News

Car insurance renewal in the UAE looks straightforward — you receive a quote, you pay, you get a new policy. In practice, six specific charges are added to most renewal invoices that expats accept without checking. Based on renewal invoices reviewed from twelve expat clients in Dubai and Sharjah during Q1 2026, the average amount paid in unjustified or avoidable charges per renewal was 680 AED. On a typical comprehensive policy costing 2,200 to 3,500 AED annually, that represents 20 to 30 percent of the total premium going to charges that were either inflated, duplicated, or entirely avoidable.

If you came from our guide on what to do when your car is impounded in UAE in the first 3 hours, you already know that traffic-related costs in the UAE add up faster than most expats expect. Insurance renewal is where the next layer of avoidable expense hides — and most of it is hidden in plain sight on the invoice.

How the UAE Car Insurance Renewal Process Works

In the UAE, motor insurance policies run for 13 months on the first purchase — covering the 12-month registration period plus one month to allow for Tasjeel renewal. After the first year, renewals are issued in 12-month cycles.

The renewal process typically happens in one of three ways:

Direct renewal with the same insurer: The insurer contacts you by SMS or email approximately 30 days before expiry with a renewal quote. Many expats renew automatically without comparing alternatives.

Renewal through a broker or comparison platform: Platforms like Bayzat or InsuranceMarket.ae generate quotes from multiple insurers simultaneously, allowing direct price comparison.

Renewal through a car service center or showroom: Some garages and dealerships offer insurance renewal as a convenience service — typically at a markup of 8 to 18 percent above direct insurer pricing.

The third route is where most hidden charges concentrate. But even direct insurer renewals carry charges that are added by default and removed only when specifically questioned.

Average comprehensive insurance premiums in UAE by vehicle category (2026 market rates):

Vehicle CategoryAnnual Premium Range (AED)Economy sedan (Toyota Yaris, Nissan Sunny)1,400 – 2,200Mid-size sedan (Toyota Corolla, Honda Civic)1,800 – 2,800Large sedan (Toyota Camry, Nissan Altima)2,200 – 3,500Mid-size SUV (Toyota RAV4, Nissan X-Trail)2,800 – 4,200Large SUV (Toyota Prado, Nissan Patrol)4,500 – 7,500

These ranges apply to GCC-spec vehicles registered in Dubai with a driver holding a valid UAE driving license. Non-GCC spec vehicles, US-spec imports, and drivers with less than two years UAE license history typically pay 15 to 35 percent above these ranges.

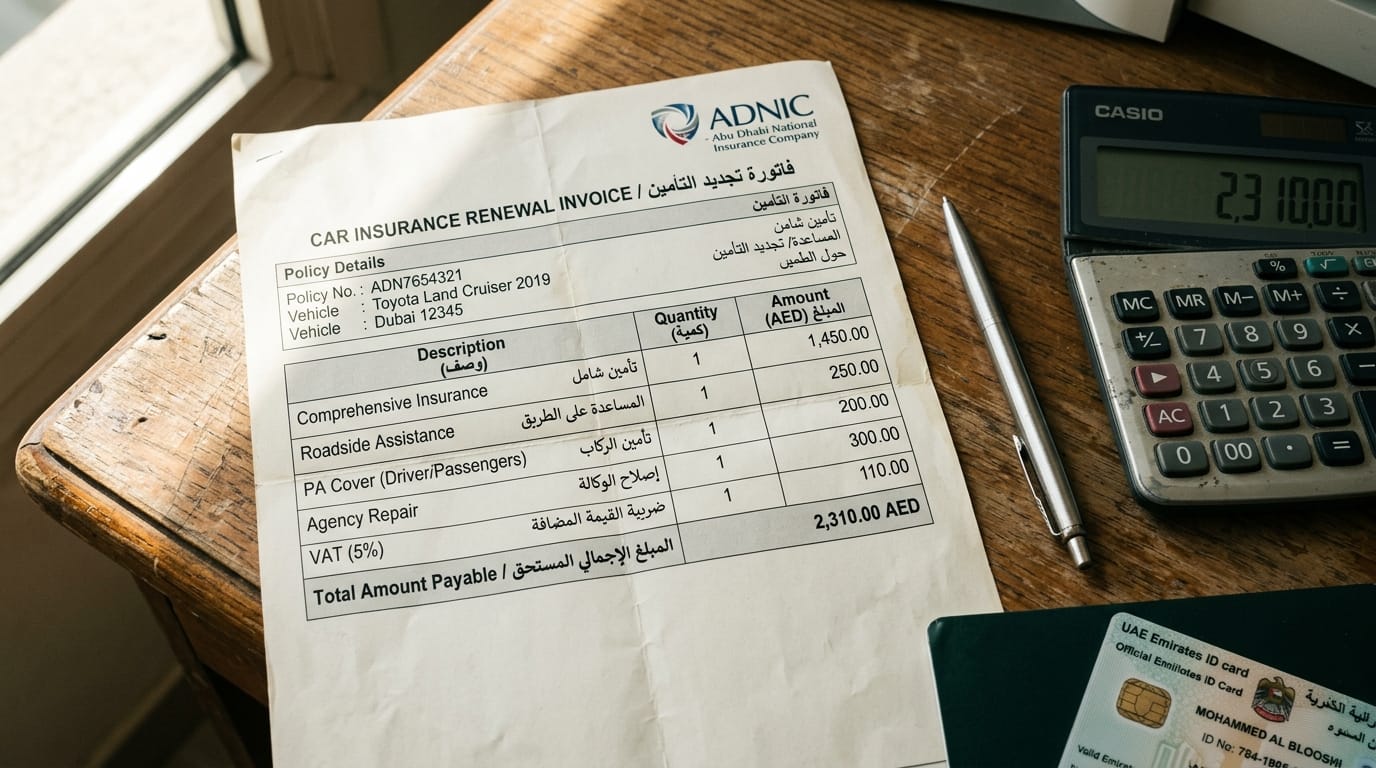

🔧 Mechanic’s Inspection Log — The Renewal Invoice That Added 920 AED

Documented case from a client consultation, February 2026, Dubai.

Client: Logistics coordinator from Manila, working in Jebel Ali on 6,800 AED salary

Vehicle: 2018 Toyota Corolla 1.6L GCC, 74,000 km

Previous year’s premium: 2,100 AED comprehensive

Renewal quote received: 3,020 AED from same insurer

The client contacted me after receiving a renewal quote that was 920 AED higher than the previous year with no explanation from the insurer. She had not made any claims during the policy year. Her vehicle had not changed. Her driving record was clean.

We reviewed the itemized renewal invoice together:

Base premium: 1,940 AED ← actually lower than the previous year due to vehicle depreciation

Add-ons included by default:

Personal accident cover for driver: 180 AED (she already had this through her employer’s group health plan — duplicate coverage)

Roadside assistance package: 220 AED (she was already enrolled in the Toyota roadside assistance program included with her vehicle purchase — duplicate coverage)

Agency repair endorsement: 350 AED (her vehicle was 7 years old — agency repair for a 2018 Corolla costs the same as a competent independent workshop for most repairs)

“Claims processing fee”: 85 AED (not a standard regulatory charge — an insurer administrative fee added by default)

VAT on the add-ons calculated on the full bundled amount rather than the base premium: 145 AED additional versus VAT on base premium alone

Total add-ons: 980 AED on top of a 1,940 AED base premium.

After reviewing each add-on, she removed the personal accident cover, the roadside assistance package, and the agency repair endorsement. She queried the claims processing fee, which was waived when questioned. The final premium was 1,940 AED plus VAT — saving 920 AED compared to the default renewal quote.

The insurer did not contact her about these removals. They processed the adjusted policy without comment. Every add-on had been added as a default.

The 6 Hidden Charges — What They Are and How to Handle Each

Charge 1 — Personal Accident Cover (PAC) Added by Default

What it is: A supplementary cover that pays a fixed amount (typically 10,000 to 200,000 AED depending on the policy) if the driver is killed or permanently disabled in an accident.

Standard cost added to renewal: 120 to 280 AED annually.

When it is legitimate: If you have no other life or disability insurance coverage. Particularly relevant for expats whose employer does not provide group life cover.

When it is unnecessary: If your employer provides group life insurance, or if you hold a personal life insurance policy that covers accidental death and disability. Most mid-to-large UAE employers provide this as standard. Check your employment contract or HR department before paying for duplicate coverage.

How to remove it: Call your insurer directly and ask to remove the personal accident endorsement from the renewal. This takes 5 minutes and reduces the premium by 120 to 280 AED.

Charge 2 — Roadside Assistance Package

What it is: A service package covering towing, battery jump-start, flat tire change, fuel delivery, and lockout assistance.

Standard cost added to renewal: 150 to 350 AED annually.

When it is legitimate: If you have no existing roadside assistance coverage.

When it is unnecessary: Toyota, Nissan, Honda, and Hyundai all include roadside assistance programs through their UAE dealer networks for vehicles within a certain age or service contract period. Many credit cards issued in the UAE — including most Emirates NBD and FAB cards — include roadside assistance as a benefit. Check both before paying the insurer for a third layer of the same service.

How to verify: Call your car manufacturer’s UAE customer service line and ask if your vehicle is enrolled in their roadside assistance program. Check the benefits section of your primary credit card. If either provides this service, remove it from the insurance renewal.

Charge 3 — Agency Repair Endorsement on Older Vehicles

What it is: A clause that guarantees your vehicle will be repaired at an authorized brand dealer rather than an independent workshop if a claim is made.

Standard cost added to renewal: 250 to 600 AED annually, depending on vehicle brand and value.

When it is legitimate: For vehicles under 3 to 4 years old, where dealer repair maintains warranty validity and uses OEM parts. For luxury vehicles where non-dealer repair has material resale implications.

When it is questionable: For vehicles above 5 years old, the difference in repair quality between a competent independent workshop (Al Quoz, Sharjah Industrial Area) and a dealer service center is marginal for most common repairs. The dealer charges higher labor rates and parts markups — which the insurer passes to the policyholder through the endorsement premium.

The specific calculation: A 2018 Toyota Corolla (7 years old in 2025) repaired at a Toyota dealer costs approximately 15 to 25 percent more than the same repair at a competent certified independent workshop. The 350 AED agency repair endorsement does not cover this difference — you pay the endorsement and the insurer still applies standard labor rate caps. The benefit is primarily psychological.

How to handle it: For any vehicle above 5 years old, request a quote without the agency repair endorsement. Compare the saving against the actual repair quality difference you expect. For most expats driving budget to mid-range vehicles over 5 years old, removing this endorsement saves 250 to 600 AED annually with minimal practical impact.

Charge 4 — Claims Processing or Policy Administration Fee

What it is: An administrative charge described variously as “policy issuance fee,” “claims processing fee,” or “administration charge” on renewal invoices.

Standard amount: 50 to 150 AED.

Regulatory status: The UAE Insurance Authority (now integrated into the Central Bank of UAE) does not mandate a standalone claims processing fee as a separate charge on motor insurance renewals. This charge is an insurer-imposed administrative fee — not a government-mandated cost.

How to handle it: When reviewing your renewal invoice, identify any line item described as an administration, processing, or issuance fee that is separate from the base premium and VAT. Ask the insurer to itemize what this fee covers. In most cases, when questioned directly, the fee is waived or absorbed into the base premium calculation. Of the twelve renewal invoices reviewed in Q1 2026, nine included this charge and seven had it removed when questioned.

Charge 5 — No-Claims Discount Not Applied or Understated

What it is: Most UAE insurers offer a no-claims discount (NCD) that reduces the base premium by 5 to 20 percent for each claim-free year, up to a maximum of typically 20 to 25 percent.

The common error: Insurers sometimes calculate the renewal premium on the previous year’s premium rather than on the base rate, which means the NCD percentage is applied to an already-inflated number. In other cases, the NCD is simply not applied to the renewal quote and the client does not notice.

How to verify: Ask the insurer for the base premium before NCD and the base premium after NCD as separate line items. Calculate the percentage reduction yourself. If you have been claim-free for two years and the discount applied is less than 10 percent, ask for a recalculation.

Typical saving when correctly applied: 150 to 500 AED depending on the base premium and number of claim-free years.

Charge 6 — Renewal Without Market Comparison

What it is: Not a specific line item — but the most expensive charge on this list. Renewing with the same insurer without obtaining competing quotes is the default behavior of approximately 70 percent of UAE expat policyholders according to industry pattern data.

The cost of auto-renewal: The average premium difference between an auto-renewed policy and the best available competing quote for the same vehicle and driver profile in UAE 2026 is approximately 300 to 700 AED annually for mid-market vehicles.

How to compare: Obtain quotes from at least three sources before renewing. The two most efficient methods:

Platform comparison through Bayzat or InsuranceMarket.ae — both generate multiple insurer quotes simultaneously within minutes using your vehicle details.

Direct comparison by calling your current insurer, one competitor insurer, and checking one comparison platform. This takes approximately 30 minutes and has a documented average saving of 380 AED per year for mid-range vehicle owners in Dubai.

Signs of a Transparent UAE Insurance Provider

Not all insurers apply these charges in the same way. Based on the twelve renewal cases reviewed in Q1 2026, these behaviors distinguish more transparent providers from those who rely on default add-ons.

They provide an itemized quote by default. A transparent insurer sends a renewal quote that separates base premium, each endorsement, VAT, and any administrative charges as individual line items — not a single total figure.

They disclose NCD percentage clearly. The no-claims discount percentage and the year it relates to are stated on the quote, not buried in fine print.

They do not add endorsements without asking. Three of the twelve renewals reviewed came from insurers who called the client before issuing the renewal quote and asked specifically whether they wanted to retain each add-on from the previous year.

They accept endorsement removals without applying pressure. A transparent insurer processes endorsement removal requests as a routine administrative task. An insurer that attempts to retain add-ons through repeated callbacks or by emphasizing worst-case scenarios every time you call is managing revenue, not serving the policyholder.

Their quotes survive market comparison. The most trusted indicator: when you obtain three quotes and the incumbent insurer’s offer remains competitive, their pricing is structured honestly. When their auto-renewal quote is 25 to 40 percent above every competitor for identical coverage, the renewal pricing was not set for competitive reasons.

The Correct Renewal Process — Step by Step

45 days before expiry: Set a calendar reminder. Do not wait for the insurer to contact you — by the time they do, you have less time to compare and they know it.

35 days before expiry: Run a comparison on Bayzat or InsuranceMarket.ae. Note the lowest three quotes for identical coverage levels.

30 days before expiry: Contact your current insurer with the competing quotes. Ask them to match or beat the best quote. Many will adjust pricing when presented with a specific competing figure — not because they cannot offer it, but because they do not offer it unless asked.

Review the itemized invoice before paying, regardless of which insurer you choose. Check for each of the six charges documented above.

Pay by credit card where possible. Several UAE banks — Emirates NBD, FAB, ADCB — offer 0% installment plans for insurance premiums on their credit cards. Splitting a 2,500 AED premium into six 0% installments costs nothing extra and preserves monthly cash flow on a standard expat salary.

FAQ — UAE Car Insurance Renewal

Understanding what you pay for insurance is one part of managing the real cost of car ownership in the UAE. The next step covers what happens when you reach the end of your ownership period and need to sell — and what the actual financial outcome looks like after two years. Read the full account: I Sold My Car in Dubai After 2 Years — Final Numbers and What I Lost

Really enjoyed reading this article. The information about car insurance was very clear and easy to understand.